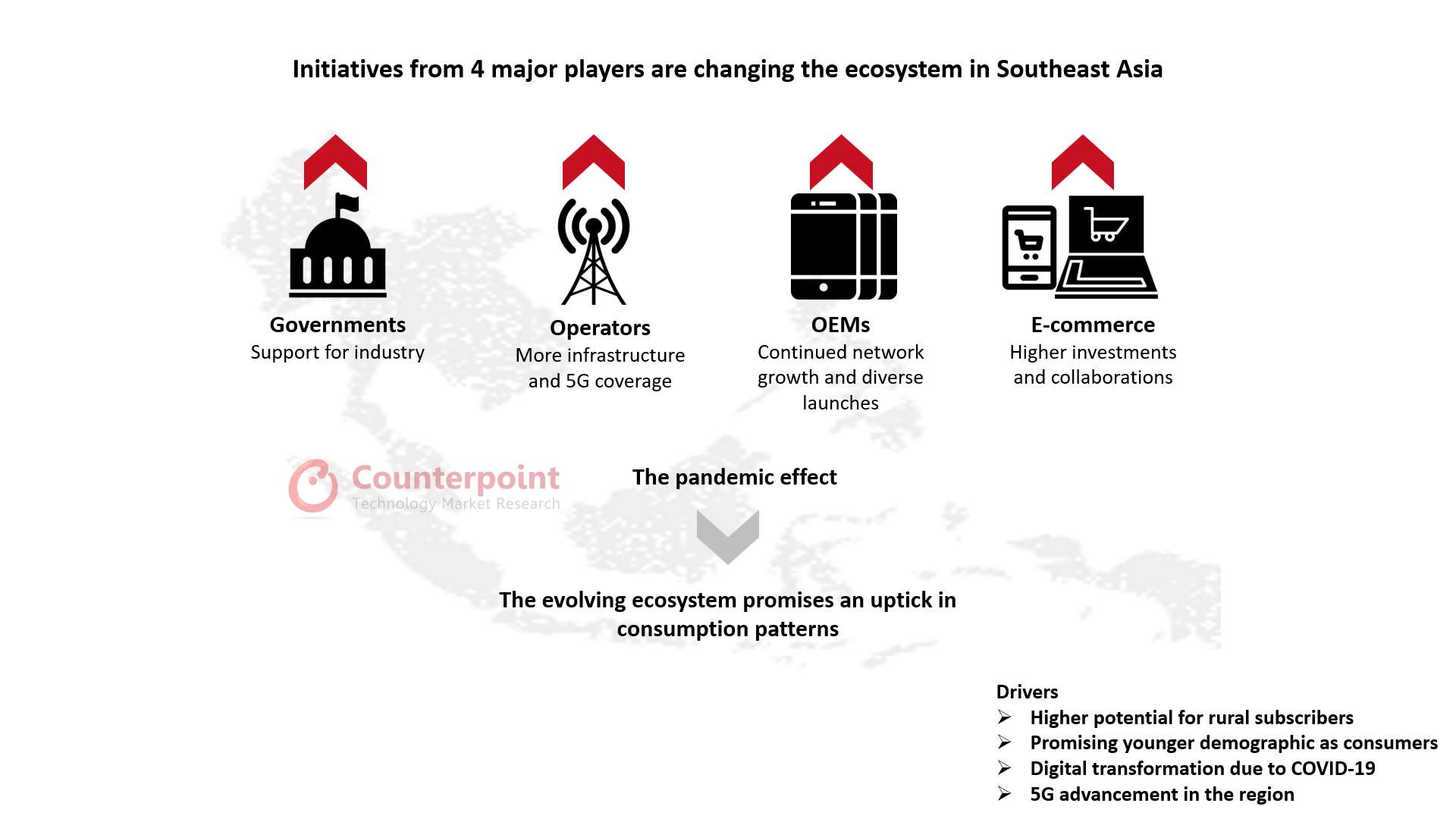

Southeast Asia (SEA) has been showing consistent economic promise for a while now. The changing landscape is giving the smartphone sector a much-needed boost as well. Four players have a pivotal role in this sector.

While government support in key SEA countries has resulted in a faster rollout of 5G infrastructure, most governments are currently focused on COVID-19 vaccination and jump-starting the economy. In the parallel, Thailand continues to concentrate on advanced 5G utilization, while countries like Indonesia, Philippines and Vietnam are focusing on solidifying their 5G infrastructure and increasing coverage.

Operators

The main operators in the key SEA countries are not only concentrating on increasing their 5G coverage but also making sure they sustain a healthy 4G network. Rural focus is helping them raise subscription levels as well. Their consistent tie-ups with OEMs are giving a push to bundled packages and 5G (especially in metros and Tier I cities). This will continue to increase at a YoY level, even after Q4 2021.

From merging telecom operators in Indonesia to industrial applications being pursued in Thailand, 5G connectivity is growing stronger in this region.

Even consumers who had not considered 5G during their most recent purchase of a smartphone, will consider it strongly in the future.

OEMs

New 5G smartphone launches in the mid-tier price band have been all the rage in this region. The ASPs for these 5G phones will go down for upcoming models from top brands like realme. This will lead to an increase in upgrades.

Brands like OPPO, Xiaomi and realme are adding consumer IoT products, like smart speakers, to purchase deals which is good exposure for their IoT portfolio in these markets. For brands like Xiaomi, the IoT segment makes up 10% of total revenue in some markets.

As the markets open, brands are also increasing their offline footprint. Xiaomi is looking to increase its sales outlets from 38 to more than 100 within this year. The brand is also making sure its after-sales network is geographically widespread. Xiaomi and realme stand out here.

E-commerce

The “9.9” shopping festival saw some big investments and celebrity endorsements on online platforms like Shopee. Other big players across SEA, like Lazada and Tokopedia, also spent on marketing campaigns and tie-ups with brands, events and celebrities.

Online sales are one of the biggest reasons for consumers to indulge in shopping towards the end of the year.

Whether it is ‘live shopping’ on Tokopedia or increasing Korean influence with music groups like BTS, consumers can relate to this association. The main SEA economies may see their highest ever online smartphone shipments in Q4 2021. With COVID-19 infection rates going down in most SEA countries, the only deterrent here is component shortages affecting supply.

Manufacturing

Q3 2021 saw governments in Indonesia and Vietnam giving emphasis to essential items. As infection rates went down in August and September, vaccination for the manufacturing sector was given priority. Starting September, most production facilities in Vietnam resumed normal operations and scaled up to make provisions for Q4 demand.

All the above factors play in favor of a very productive and lucrative smartphone season in Q4 2021. All key SEA countries are likely to show more than 20% growth over Q3 2021 and a healthy YoY increase as well. Indonesia, Thailand and Philippines will show a higher online share in smartphone shipments.