AMD reported a 23% year-on-year (YoY) decline in revenues in Q1 2019, making it the third consecutive quarter of declining revenues. AMD’s topline suffered due to the declining sales of Radeon channel products as well as decreased demand from Taiwan and Chinese OEMs/ODMs. However, its operating margin grew by 5 percentage points on account of increasing sales of EPYC, Ryzen, and datacenter GPU products.

Key highlights:

- AMD reported revenues of US$1.27 billion, down 23% YoY and 10% QoQ. Gross margin came in at 41%, a 5 percentage point increase YoY. Cash, cash equivalents and marketable securities stood at US$1.19 billion.

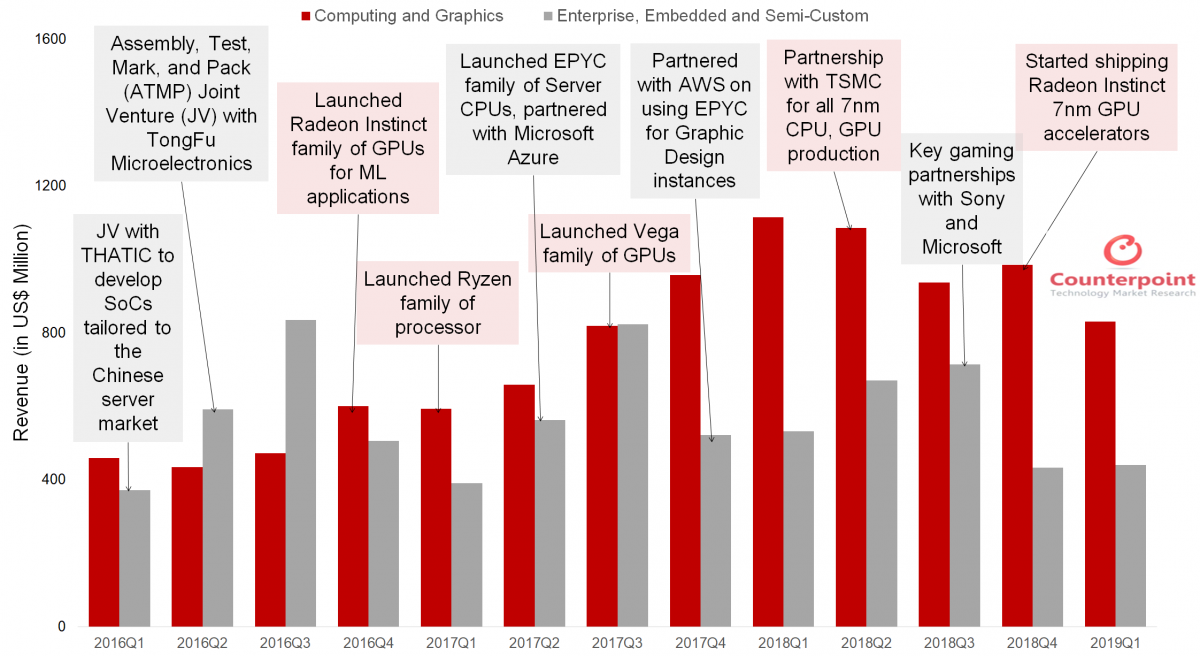

- Computing and Graphics segment (client solution processors and all GPUs) net revenue was US$831 million, down 26% YoY. Client Processor ASP was up YoY driven by Ryzen processor sales. GPU ASP was up due to datacenter GPU sales.

- Enterprise, Embedded, and Semi-Custom (custom-made solutions and datacenter CPUs) net revenue was US$441 million, down 17% YoY. However, EPYC processor sales saw an increase.

- International Sales accounted for 77% of total revenues for Q1 2019 as compared to 82% in the same period the previous year.

- Research and Development expenses climbed to US$373 million, an increase of 9% YoY. AMD also said that 7nm product launches are on track.

- AMD amended its WSA (Wafer Supply Agreement) with GlobalFoundries, which allows the company to award contracts to any foundry for their 7nm and thinner nodes.

Counterpoint’s View:

- AMD’s Q1 2019 results are a mixed bag. While revenues are down, margins have gone up. Recent offerings, such as Radeon Instinct datacenter GPUs as well as Ryzen processors, are the key reasons for the high margins. An improved product mix is also aiding AMD.

- AMD is heavily banking on the new launches in Q3 2019. These new launches include the new 7nm Navi GPUs and Rome (EPYC 2) server processors with Zen 2 microarchitecture. AMD has the upper hand on the technology front as Intel will not be able to ship 10nm chips until late 2019.

- AMD is continuously working on building strategic partnerships, which will prove beneficial to the fabless chip maker in the long run. Google has partnered with AMD to use the AMD Radeon datacenter GPUs for the Stadia gaming platform. AWS launched three new EPYC processor powered EC2 instances.

- Financially, the company is performing better. Cash and cash equivalents stood at US$1.19 billion, up from US$1.16 billion in the previous quarter. Total debt was US$1.09 billion, down from US$ 1.25 billion in the last quarter.

- AMD’s amended wafer supply agreement (WSA) with GlobalFoundries will allow the chip maker to expand its partnership with TSMC for sourcing out 7nm based chips. However, according to the agreement, AMD has to pay if it fails to meet the annual wafer purchase target for 2019-21 which poses an operational risk considering its heavy emphasis on the 7nm technology.

- The semiconductor industry had witnessed talent wars over time. In the last two years, Intel has poached three high-level executives from AMD, namely, Raja Koduri (previously SVP, Radeon in AMD), Chris Hook, and Jim Keller (responsible for designing the Zen architecture). AMD has to work on retaining talent to win over the competition in the long run.

Rise from the ashes: Chronology of AMD’s growth from recent history

Expectations for Q2 2019:

- AMD’s Q2 revenue guidance is US$1.52 billion, which is 19% up QoQ and down 13% YoY. However, due to the new launches in Q3 2019, customers may end up waiting for the better 7nm offerings, which may lower sales for the second quarter.

- Blockchain and client GPU products’ sales will continue to dip due to slower demand. Semi-custom revenue will stabilize in the second quarter. However, datacenter GPUs and Ryzen processor will drive up the sales. The unit ASP for processors and GPUs are expected to increase.

- In addition to cloud, building channel partnerships as well as a direct sales force for enterprise sales is a major concern to drive up the revenue in the Enterprise space.