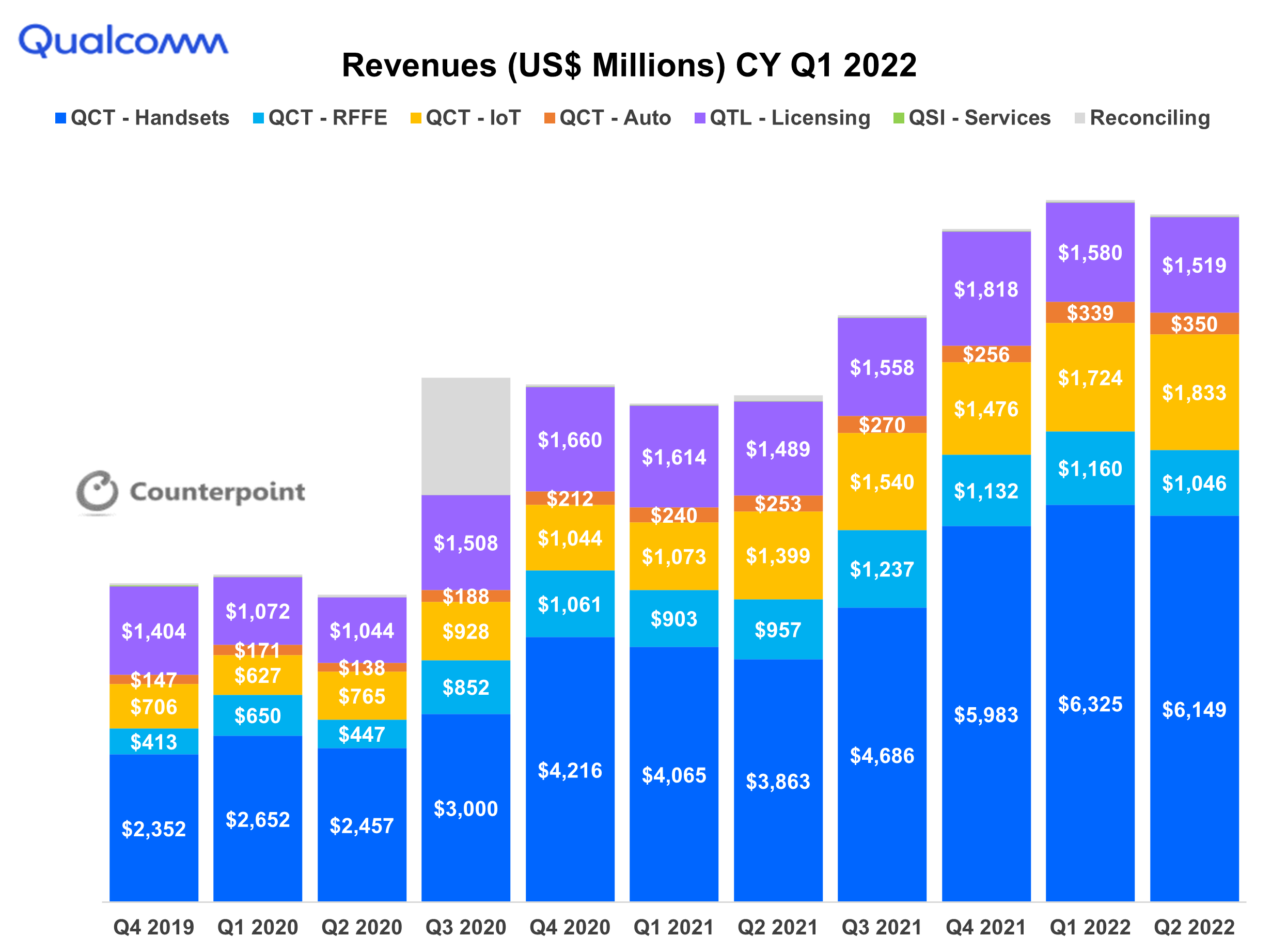

Despite macroeconomic headwinds and investors’ angst with a declining smartphone market, Qualcomm reported great quarterly results. Qualcomm was aided by its one technology roadmap which connects the intelligent edge, even during a weak smartphone market. There were two major stories of the quarter. First, despite a shrinking smartphone market, which Counterpoint Research Market Outlook predicts will decline by 3% in 2022, Qualcomm’s handset business grew a whopping 59% YoY. Despite weakness in the low and mid-tier smartphone market written often about within Counterpoint Research, Qualcomm benefitted from its focus on the high-tier and a favourable mix of handset chips.

The second large story of the quarter was that Samsung and Qualcomm inked a licensing agreement through 2030 and the 6G era. Qualcomm will power future Galaxy devices with high-end Snapdragons within smartphones, PCs, tablets, and XR. Qualcomm’s percentage of Galaxy devices will likely continue to grow. Note that Qualcomm is currently designed into about 75% of the Galaxy S22 family. Qualcomm specifically highlighted that the same royalty terms are in place. This means it is highly likely other OEMs will agree to the same royalty terms upon renewal. Huge win for Qualcomm.

Source: Qualcomm Investor Relations

Other highlights from the quarter:

- The design wins within automotive continue. Its digital chassis solutions revenue pipeline increased to $19 billion, up $3 billion YoY. Its latest design win is CARIAD, Volkswagen Group’s software company. CARIAD will use Qualcomm’s system-on-chips (SoCs) to enable its assisted and automated driving functions up to Level 4. This solution delivers 700 TOPs (trillions of operations per second).

- IoT revenues grew 31% YoY driven by edge networking and industrial IoT with combined revenue growth of more than 40%. Qualcomm will profit from the growth of Windows on Snapdragon and ARM-based computing. There are over 225 enterprise companies, more than 100 ISVs, and over 15 channel partners supporting the Snapdragon compute platform. Price points and performance continue to expand the value proposition. Further edge networking, Wi-Fi 7, and the robotics platform will be a key segment for growth for IoT.

- Qualcomm recently announced a new wearables platform, which saw a large leap in specs. Briefly, it is built on a 4nm process, 50% lower power consumption, 2x performance, and 30% smaller size. This redesign will push more processing to the co-processor. The power upgrade vastly helps kids/senior watch space. 4nm & performance will enable new sensors and the high-end. This will vastly help the smartwatch space allowing for better tracking (think kids/seniors), better health monitoring, and new applications in development. It remains a hurdle that too often the smartwatch is on the charger and not collecting data on the wrist. Qualcomm’s solution will greatly help this. OEMs will be able to scale with two platform options. There are 25 design wins and growing.

- RFFE grew 9% on an annual basis and will be a key part of Qualcomm’s diversification strategy. A large share of the Qualcomm RFFE is driven by smartphones. As per Counterpoint’s Smartphone RFFE Revenue report, Qualcomm led the smartphone RFFE market with 23.5% in Q1 2022. Qualcomm has a complete modem-to-antenna solution for 5G thereby supplying the end-to-end needs of smartphone OEMs. In the coming years, RRFE growth will come from Auto and IoT. The current RFFE design pipeline for the automotive segment is around $900 million. Also, in IoT, there is an opportunity for next-generation Wi-Fi (Wi-Fi 7) and Bluetooth for RFFE modules. The ASP growth in RFFE content from mid-end to premium smartphones is less when compared to mid-end and premium smartphone chipsets.

- There were limited comments about Qualcomm’s move into open, virtualized 5G RAN. However, the company recently announced partnerships with Hewlett Packard offering a next-gen 5G virtual DU solution. Qualcomm’s differentiation is lower power requirements, which the company explains are 60% lower for operators. The move to open RAN will likely be a rolling change with potentially more of a shift during the 6G transition.

- Qualcomm guided Q3 2022 revenues in the range of $11 billion to $11.8 billion driven by the Auto and IoT segment in QCT. Considering the global macro-economic conditions and the slowdown in consumer product purchases, Qualcomm’s forecast for the handset has been reduced to mid-single digits. Qualcomm can mitigate revenue declines if the premium segment performs much better than the low and mid-tiers.

Revenue growth this quarter was driven by the handsets due to a higher premium mix, automotive was driven by the digital cockpit solution, and demand in edge networking and industrial IoT in the IoT segment. Looking at the second half of 2022, handsets may be affected by slowing consumer demand, similar to some applications in consumer IoT. But, automotive and IoT (industrial and edge) will continue to drive growth.