- The global cellular IoT module market’s shipments declined 2% in 2023 as compared to 2022.

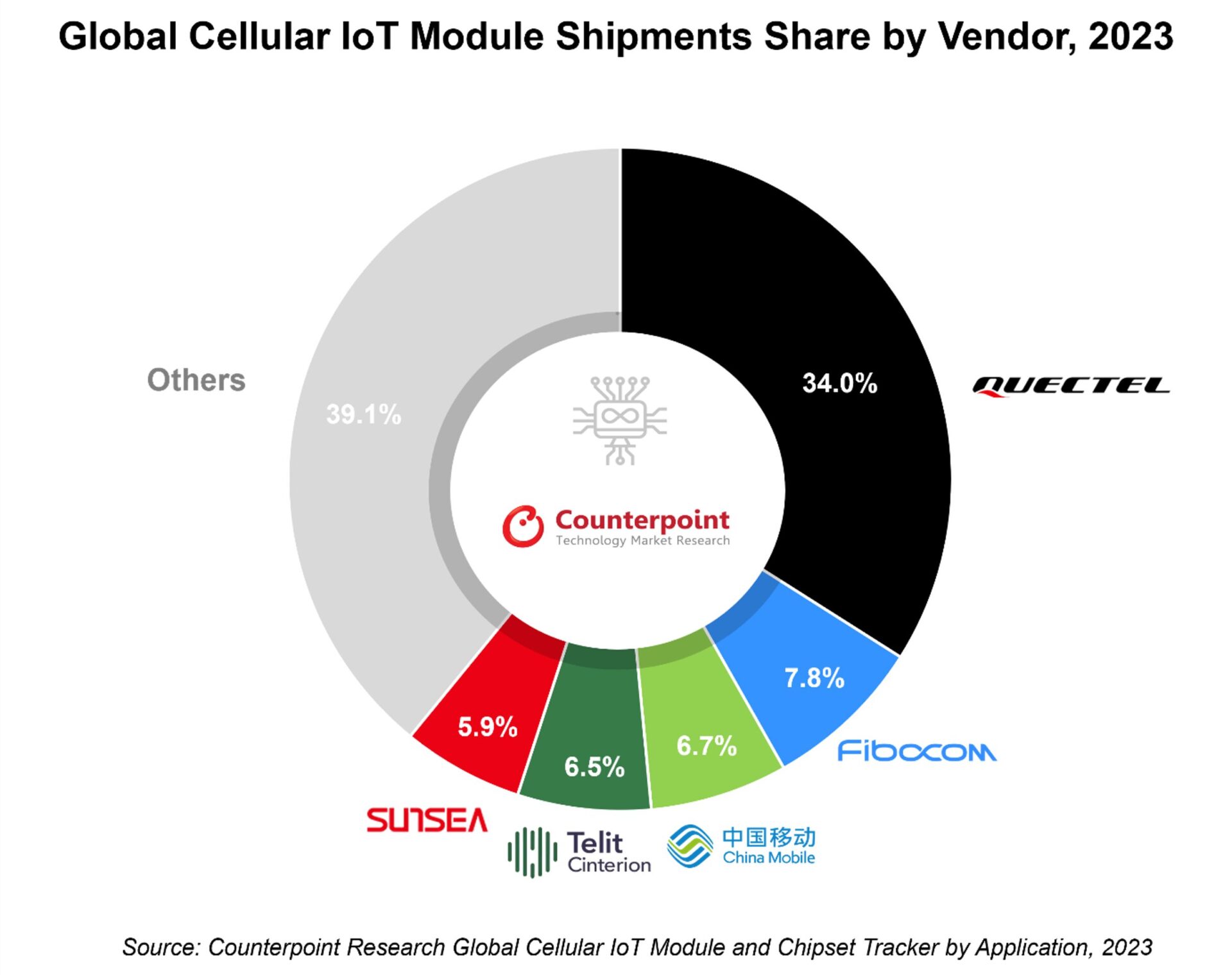

- Despite a decline in shipments, Quectel continued to lead, followed by Fibocom and China Mobile.

- NB-IoT and 4G Cat 1 shipments declined in its top market, China, where 4G Cat 1 bis gained at 4G Cat 1 and NB-IoT’s expense.

Seoul, Beijing, Boston, Buenos Aires, Hong Kong, London, New Delhi, San Diego – March 21, 2024

Global cellular IoT module shipments saw their first-ever annual decline in 2023, falling 2% YoY, according to Counterpoint’s latest Global Cellular IoT Module and Chipset Tracker by Application report. Inventory adjustments following supply chain disruption and reduced demand in some key market verticals like industrial and enterprise were some of the key factors driving this decline.

4G Cat 1 bis grew the fastest in 2023, capturing over 22% of the shipments. In China, 4G Cat 1 bis has now become the primary cellular standard for POS, smart meter, telematics and asset tracking markets, owing to its affordability and energy efficiency. The market is slowly transitioning from 4G Cat 1 and NB-IoT to more efficient 4G Cat 1 bis.

Commenting on market dynamics, Associate Director Mohit Agrawal said, “India and China have shown positive growth due to increasing demand in the smart meter, POS and asset tracking markets. Conversely, the rest of the world witnessed a sharper decline, indicating a lack of expected market momentum.”

Agrawal added, “Around 12% of the modules shipped in 2023 were equipped with AI capabilities at the software or hardware level. These modules are gaining popularity in high-end markets such as automotive, router/CPE and PC, facilitating the management of the escalating data load in these sectors.”

- Quectel, the leading module vendor, experienced a decline in its market share primarily because of weakened demand in markets outside China. The company has partnered with Syrma SGS Technology to manufacture IoT modules in India.

- China Mobile and Fibocom experienced double-digit YoY growth. China Mobile’s growth was driven by smart meters, asset trackers and POS applications, while Fibocom’s growth was driven by POS and telematics applications.

- This year’s merger between Telit and Thales propelled Telit Cinterion into the top five vendors of IoT modules. To further solidify its presence in India, Telit partnered with VVDN for local production.

- Several Chinese brands like Unionman, OpenLuat, Lierda and Neoway have shown significant growth within specialized markets like smart meter, asset tracking and POS.

Commenting on the market outlook, Research Analyst Anish Khajuria said, “In 2024, the IoT module market is expected to return to growth in the second half of the year with normalizing inventory levels and increasing demand in the smart meter, POS and automotive segments. Moreover, substantial growth is forecasted for 2025, coinciding with the widespread adoption of 5G and 5G RedCap technologies in smart meters, routers/CPE, POS systems, automotive solutions, and asset tracking applications.”

For detailed research, refer to the following reports available for subscribers:

- Global Cellular IoT Module and Chipset Tracker, Q4 2023

- Global Cellular IoT Module and Chipset Tracker by Application, Q4 2023

Counterpoint tracks 1,500+ IoT module SKUs on a quarterly basis and provides forecasts on shipments, revenues and ASP performances for 80+ IoT module vendors, 12+ chipset players and 18+ IoT applications across 10 major geographies.

Background

Counterpoint Technology Market Research is a global research firm specializing in products in the technology, media and telecom (TMT) industry. It services major technology and financial firms with a mix of monthly reports, customized projects and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

Follow Counterpoint Research

press(at)counterpointresearch.com

![]()