![]()

Economic data:

• Inflation falling faster than expected in the US and Europe. Interest rates peaked in Q4 2023, with potential rate cuts by mid-2024.

• Continued US consumer strength, supported by a strong job market.

Tech Sentiment:

• Tech outlook continues to improve after earnings season, due to better growth prospects and AI frenzy.

• Much improved semiconductor numbers paving the way for a rebound in consumer electronics in 2024.

International Politics:

• High-level meetings between US and Chinese officials signal a willingness to prevent further fallout.

Domestic politics in the West:

• The US entering a highly combative electoral cycle.

• European governments struggle to contain the rise of far-right and internal disputes.

China:

• Economic data disappoint.

• Souring business and consumer sentiment, with few signs of stimulus measures.

Geopolitical conflict:

• The Russia-Ukraine war drags on. War fatigue could see the West withdraw support for Ukraine.

• The Gaza War risks spreading across the Middle East.

• Supply chains disrupted due to attacks in the Red Sea.

![]()

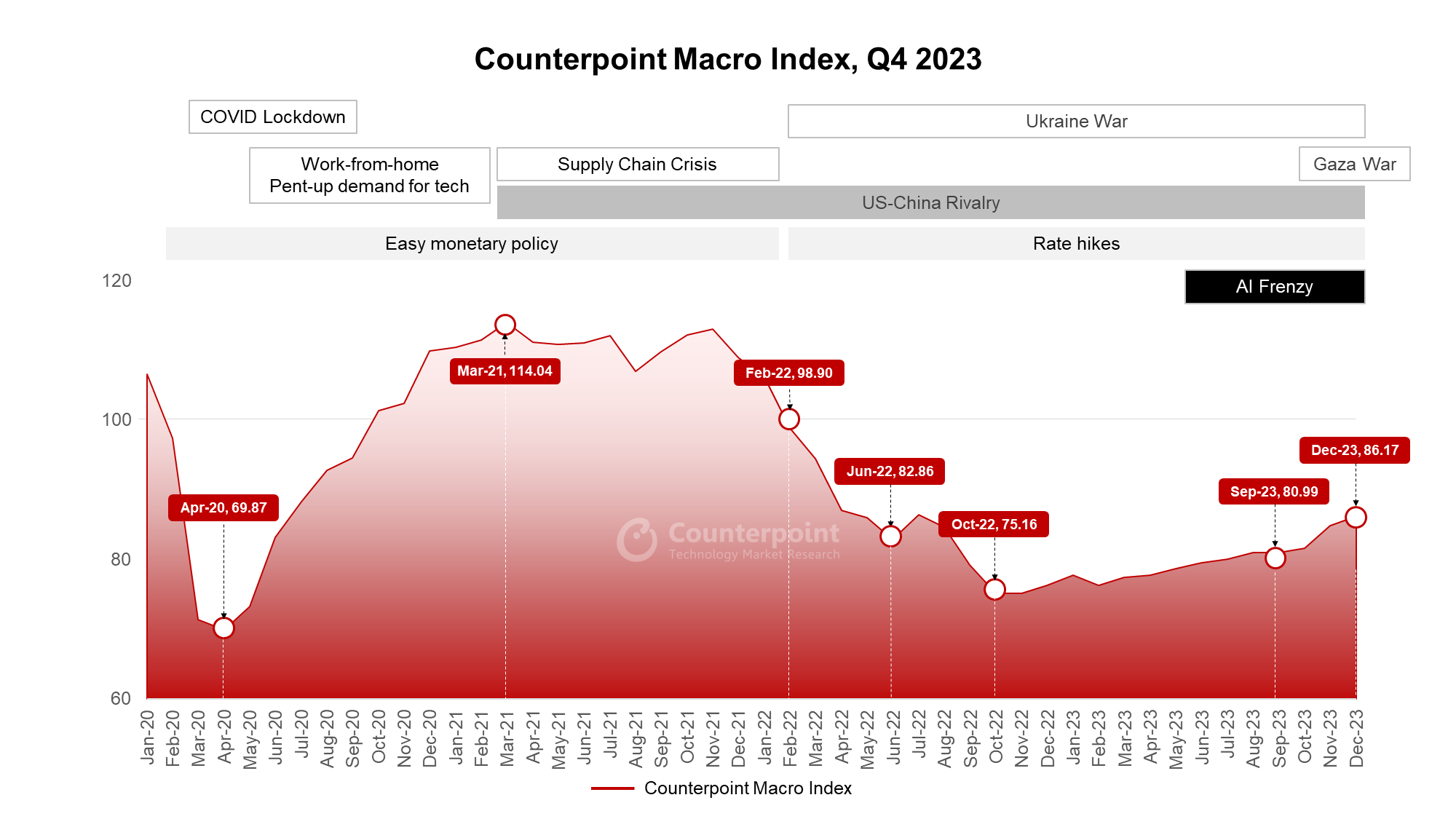

• Recovery accelerated in Q4 2023; Positive momentum to continue through 2024.

• Q4’s one-year forecast has been upgraded from Q3’s due to much better economic numbers.

• Economic data recovery to continue, but global growth prospects are under pressure.

• Main story of recovery due to lower inflation and interest rates to remain intact.

The rise of many secondary risks:

• 2024 is a massive election year: More than half of the world’s population, in more than 50 countries.

• US politics impacting global trade relationships.

• Appetite for consumer tech spending could remain weak, particularly if AI disappoints.

• China facing serious structural issues.