- Denso’s Q4 revenue boosted by strong car sales in Japan and North America.

- Denso makes upward revision to FY2024 revenue forecast provided in Q3 2023.

- Denso set to benefit from rising adoption of smart EVs in China, the US and SEA.

- Denso is focusing on rebuilding trust with domestic manufacturers before expanding to target international players.

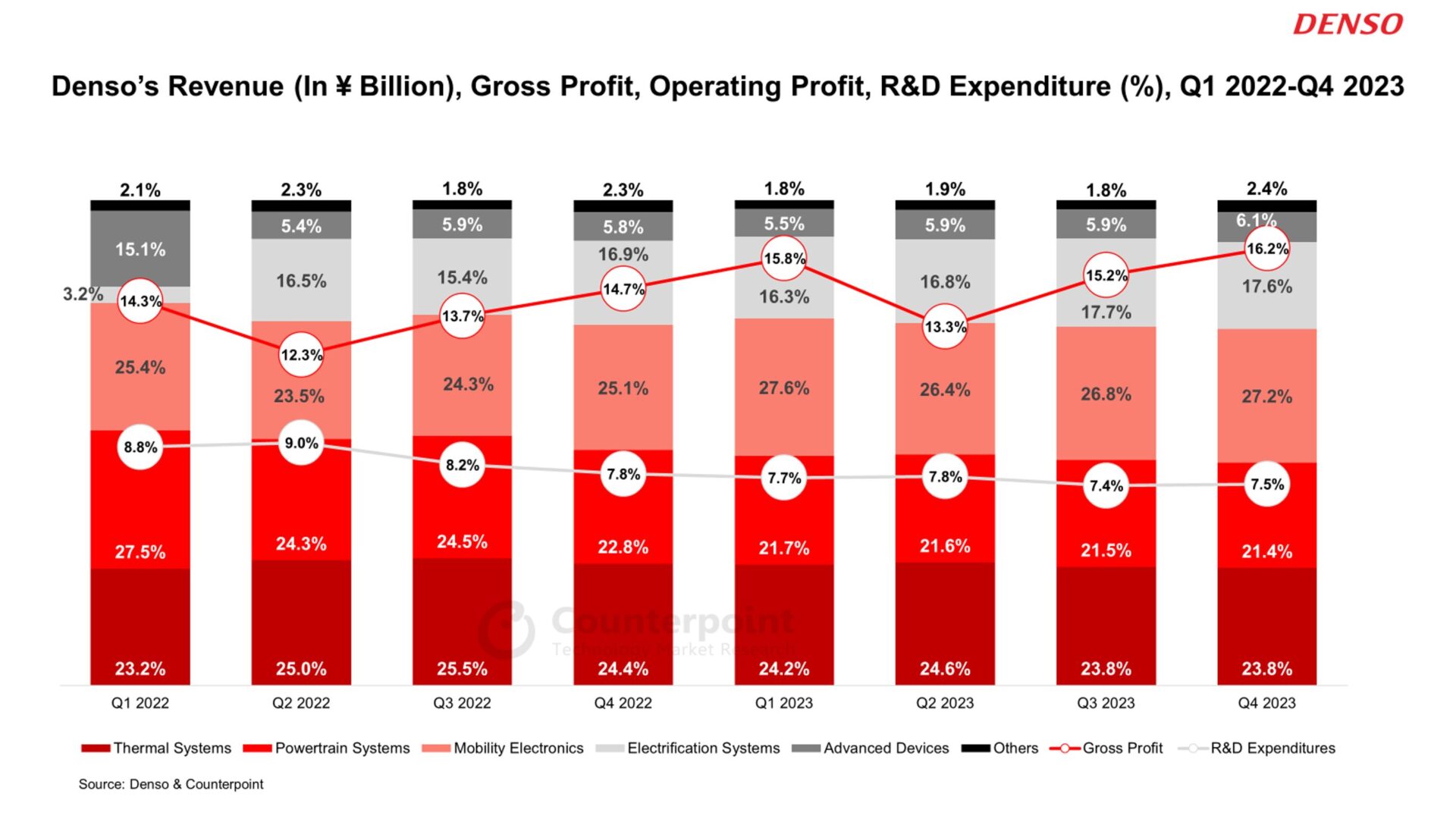

Automotive components maker Denso Corporation posted a 14% YoY rise in Q4 2023 revenue, driven by the strong sales of cars using its thermal systems, powertrain systems, electrification systems and mobility electronics in Japan and North America. Additionally, Denso and Toyota Group’s strong collaboration contributed to over half of Denso’s total automotive group revenue during the quarter. The Q4 2023 results highlight Denso’s strong financial position and solidify Denso’s pivotal role in manufacturing essential automotive components.

However, the company’s operating profit declined 76% YoY in Q4 2023 due to a rise in material costs, particularly for electronic components, and the additional provision made for quality assurance.

Denso on Toyota Group Vision:

Denso: “We take the Toyota Group Vision very seriously because we have caused the quality issues. We have been stating our ‘DENSO of Quality’, but we are strongly aware that this has been wavered. With the priority on returning to our roots and regaining trust and credibility, we would promote the systematization of quality control and initiatives for ‘awareness’, ‘knowledge’, and ‘culture’.”

Soumen Mandal’s Analyst Take: Denso acknowledges its mistakes and is diligently working to rectify them, which is crucial for maintaining transparent and strong relationships with customers. Prioritizing quality ensures they regain trust across all stakeholders.

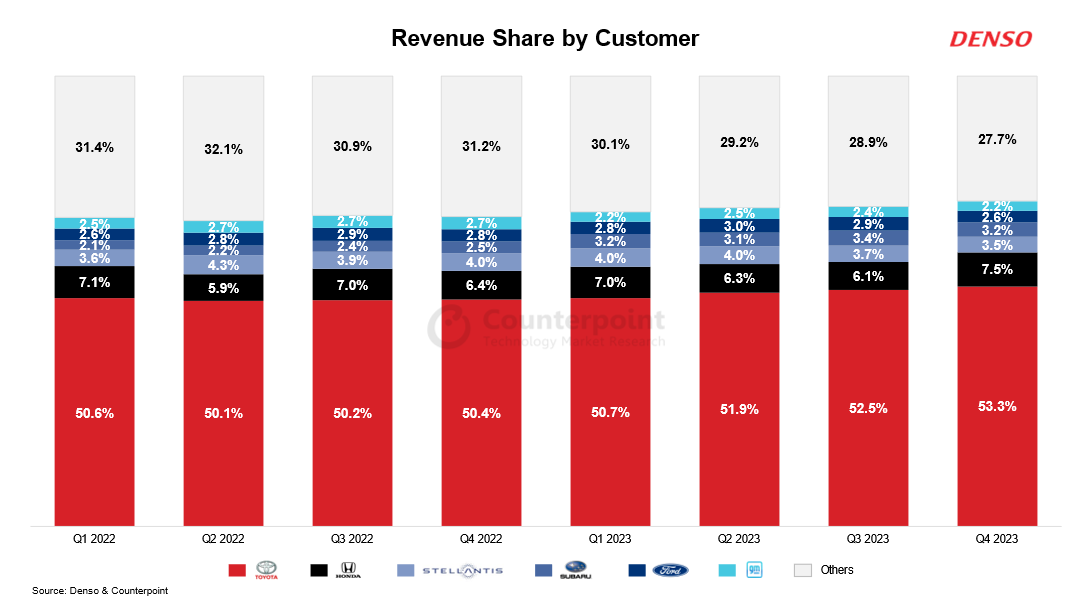

Domestic automakers such as Toyota, Honda, Subaru, Suzuki, Mazda, Nissan, and Mitsubishi collectively account for over 70% of Denso’s total automotive group revenue. Therefore, Denso is focusing on rebuilding trust with domestic manufacturers before expanding to target international players. This approach appears sustainable, especially during the ongoing transition in the automotive industry.

Denso: “Overall, we feel like the number of vehicle production has returned to a slightly inferior level from the pre-Corona level. As for downside risks, China is extremely large, and although sales decreased by about 10% in December, we think that inventory adjustments would begin in the future, and we think that sales would be 2%-3% lower than the sales plan in the fourth quarter. In the ASEAN region, vehicle production seems to have stopped declining, but we think that sales would continue to be about 10% lower than the sales forecast due to the decline in sales of pickup trucks in Thailand and the continued tightening of loan lending standards.”

Soumen Mandal’s Analyst Take: Car sales are on the rise, and while Counterpoint expects them to return to pre-COVID-19 levels by 2025, the long-term outlook remains optimistic. The expanding market for electrification and ADAS is expected to drive growth in the automotive industry.

Denso’s focus outside of Japan lies in the crucial regions of Asia and North America. The increasing adoption of smart EVs in China, the US and SEA regions, is poised to foster healthy growth for the brand in the future.

Result Summary:

- Revenue Highlights:

- Denso’s revenue jumped 14% YoY in Q4 2023, driven by strong car sales in Japan and North America. Additionally, foreign exchange rates provided a boost and expanded its offerings in electrification, safety, and comfort features.

- Denso’s automotive revenue grew 15.4% YoY in Q4 2023, driven by increased demand, strategic partnerships, and focus on innovative products.

- Denso’s non-automotive business experienced a 38.5% YoY revenue decline in Q4 2023. This could be due to Denso’s focus on strengthening its core automotive business due to which the company may have neglected its other operations.

- Key Contributors: Denso’s thermal systems, powertrain systems, and mobility electronics contributed to more than 70% of the total group revenue. Mobility electronics was the fastest-growing segment in Q4 2023 while the electrification systems segment witnessed the highest growth over the last two years.

- Risk: Japan contributed to nearly 60% of Denso’s total revenue as the company’s major customers are Japanese OEMs. Denso can look for globalization for the next phase of growth and remain competitive against international players such as Continental, Bosch, ZF and BorgWarner.

- R&D Expenditures: By prioritizing R&D, Denso maintained consistent investment in research and development. This shows that they are committed to finding new solutions and advancing car technology to grow in the future.

- Operating Profit: Denso’s operating profit experienced significant fluctuations, peaking at ¥158.2 billion in Q1 2023 before declining steadily to ¥26.8 billion in Q4 2023. This represents an overall downward trend, despite strong initial performance.

Outlook:

Denso is expanding its product range to align with the transition towards electric autonomous mobility, while also restructuring its business operations to meet rising demand. Denso’s Hungary plant is focused on customers beyond Toyota, indicating Denso’s readiness for geographical expansion.

Denso revised its FY2024 revenue forecast upward to ¥7120 billion from the earlier guidance provided in Q3 2023, prompted by a positive outlook for vehicle sales, along with increased production of electrification and advanced safety systems. With Japanese auto OEMs recovering from the impact of COVID-19 and embracing newer technologies to remain competitive against Chinese and European OEMs, the future appears promising for Denso.