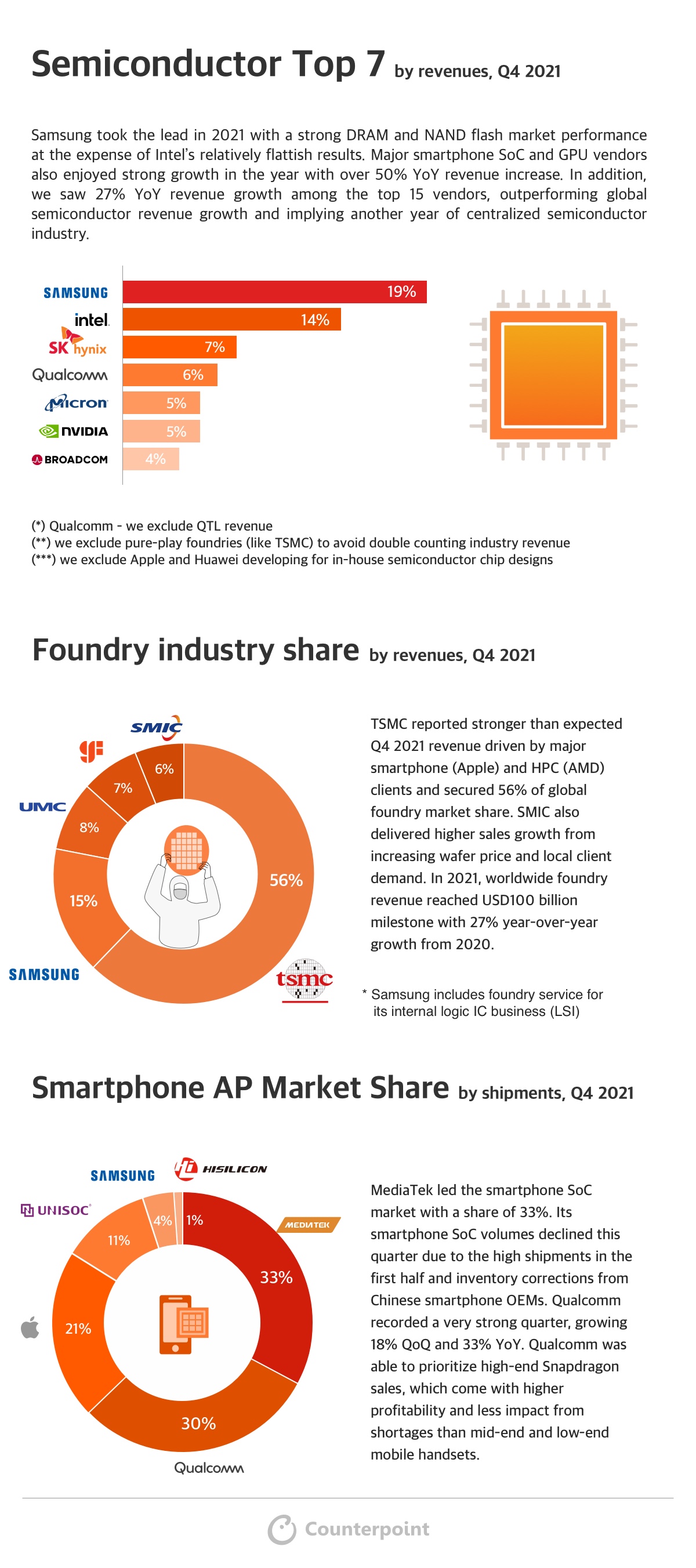

Semiconductor Top 7 by revenues, Q4 2021:

Samsung took the lead in 2021 with a strong DRAM and NAND flash market performance at the expense of Intel’s relatively flattish results. Major smartphone SoC and GPU vendors also enjoyed strong growth in the year with over 50% YoY revenue increase. In addition, we saw 27% YoY revenue growth among the top 15 vendors, outperforming global semiconductor revenue growth and implying another year of centralized semiconductor industry.

Foundry Industry Share by revenues, Q4 2021

TSMC reported stronger than expected Q4 2021 revenue driven by major smartphone (Apple) and HPC (AMD) clients and secured 56% of global foundry market share. SMIC also delivered higher sales growth from increasing wafer price and local client demand. In 2021, worldwide foundry revenue reached USD100 billion milestone with 27% year-over-year growth from 2020.

Smartphone AP Market Share by shipments, Q4 2021

MediaTek led the smartphone SoC market with a share of 33%. Its smartphone SoC volumes declined this quarter due to the high shipments in the first half and inventory corrections from Chinese smartphone OEMs. Qualcomm recorded a very strong quarter, growing 18% QoQ and 33% YoY. Qualcomm was able to prioritize high-end Snapdragon sales, which come with higher profitability and less impact from shortages than mid-end and low-end mobile handsets.

Use the button below to download the high resolution PDF of the infographic: